It’s 9 p.m. on a Tuesday, and your sister is standing in your kitchen with her phone in one hand. She’s trying to figure out which company insures the car your dad just totaled, what his cardiologist’s name is, and whether the mortgage comes out of autopay or a checkbook she now has to find. You’re at the hospital with him and not answering texts. She isn’t falling apart because something terrible happened — she’s falling apart because every piece of information that would make the next 48 hours manageable lives in your head, your phone, and a drawer she’s never opened.

Here’s the reframe most people miss: being prepared is not a feeling. It’s a file. That file is a family emergency binder — and it’s the single most useful thing you can build this weekend. Peace of mind isn’t a state of mind you slowly arrive at; it’s something a specific person can open, read, and act on when you can’t.

What a family emergency binder actually is

A family emergency binder is a single, organized collection — physical, digital, or both — of the documents, accounts, contacts, and instructions someone would need to step into your life and keep it running if you couldn’t do it yourself.

It is not a doomsday-prepper kit, and it’s not just a will. Think of it as the operating manual for your household. The real test isn’t “do I have my documents somewhere?” It’s this: if you were unreachable for two weeks, could someone you trust pay your bills, reach your doctors, find your insurance policies, and care for your kids or pets — without guessing and without you?

For most families, the honest answer is no. And the gap isn’t about caring. A 2024 Caring.com survey (opens in new tab) found that 64% of Americans believe having a will is important, but only 32% actually have one. That gap — between knowing something matters and having it ready — is exactly the gap an emergency binder closes. A will is one page of a much bigger picture, and the picture is what your family will be staring at during the worst week of their year.

Why “I’ll get to it” is the most expensive plan

Emergencies don’t schedule themselves around your free Saturdays. The whole reason this document is worth building is that you can’t build it in the moment you need it — by definition, the person who knows where everything is has become unavailable.

When the information isn’t gathered, the cost lands on someone else, usually at the worst possible time:

- Hours lost to scavenger hunts. Logins, policy numbers, and account balances get reconstructed from scratch by people who are also grieving, frightened, or exhausted.

- Money left on the table. Life insurance that no one knew existed. A subscription that keeps charging a closed estate. A tax document that surfaces a year too late.

- Decisions made blind. Without an advance directive or a note about your wishes, the people who love you are forced to guess what you’d want — and then live with the guess.

A binder doesn’t prevent the emergency. It removes the second emergency: the frantic, avoidable search for information that you already had.

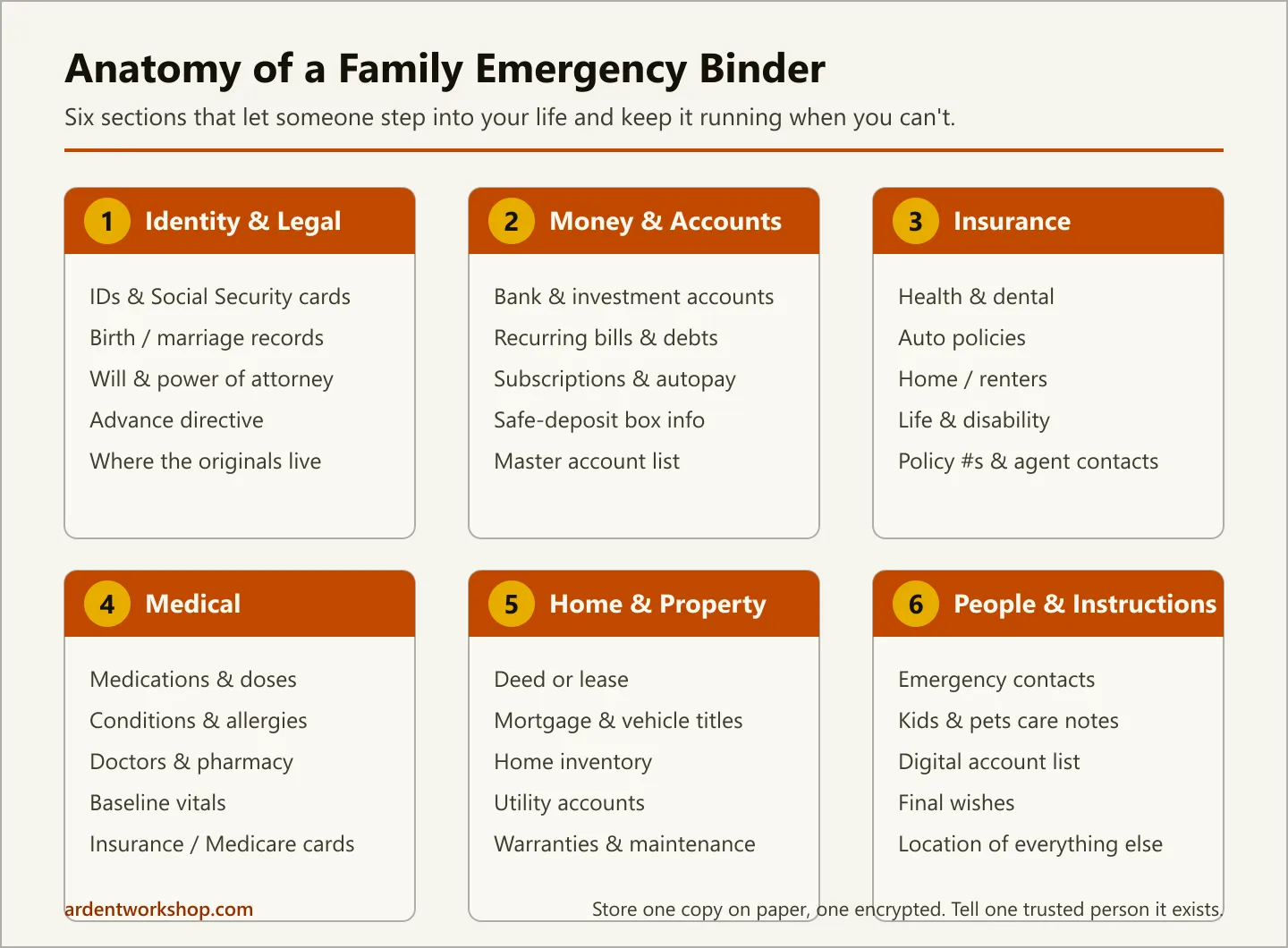

What goes in a family emergency binder: the six sections

The fastest way to make this feel doable is to stop thinking of it as one giant project and start thinking of it as six small ones. Build it section by section. Here’s the full map of what belongs in each — and, just as important, where the original of each item should live.

| Section | What to include | Where the original lives |

|---|---|---|

| 1. Identity & Legal | Birth/marriage certificates, Social Security cards, passports, will, power of attorney, advance directive/living will, citizenship or military records | Fireproof safe or attorney’s office; binder holds copies + a note on location |

| 2. Money & Accounts | Bank and investment accounts, recurring bills, subscriptions, loans and debts, autopay setup, safe-deposit box info | Binder holds the master list; statements stay with institutions |

| 3. Insurance | Health, auto, home/renters, life, and disability policies with policy numbers and agent contacts | Binder holds policy summaries + contact info |

| 4. Medical | Current medications and doses, conditions, allergies, doctors, pharmacy, baseline vitals, advance directive, insurance/Medicare cards | Binder holds the summary sheet; advance directive original with attorney/doctor |

| 5. Home & Property | Deed or lease, mortgage details, vehicle titles, home inventory, utility accounts, maintenance and warranty records | Titles/deeds in safe; binder holds copies + the home inventory |

| 6. People & Instructions | Emergency contacts, instructions for kids and pets, list of digital accounts, funeral/final wishes, location of everything not in the binder | Binder is the home for all of this |

That table is the whole post in one grid — and the visual below is the same six sections at a glance, so you can see the shape of the binder before you build it.

Start with the one-page version first

If six sections still feels like a lot, build the minimum viable binder first — a single page that covers the questions someone will ask in the first hour, not the first month. Everything else can be filled in later. This starter page should answer:

- Who are the three people to call first, and what are their numbers?

- Where are the originals of the will, advance directive, and IDs?

- What medications does each person take, and who are their doctors?

- Which accounts cover the mortgage/rent and the main bills, and how are they paid?

- Who takes the kids and the pets, and what do they need to know today?

If you only ever finish that one page, you’ve already removed most of the panic from a bad night. The rest of the binder is just turning each of those answers into a section.

Where it should live — and who can open it

A binder no one can find is just a tidy version of the problem. Two rules make it usable:

- Keep it in two forms. A physical copy in a fireproof, water-resistant box at home, and a digital copy (encrypted folder or password manager) that updates more easily. Paper survives a dead phone and a power outage; digital survives a house fire. You want both.

- Tell a trusted person it exists and how to reach it. This is the step people skip, and it quietly defeats the entire project. At least one person outside your own head needs to know the binder exists, where it is, and how to get into it.

A word on security: the binder should point to your passwords, not necessarily contain them. Store credentials in a dedicated password manager and note in the binder how your trusted person can access that manager (or your bank’s “legacy contact” or “trusted access” feature). Loose passwords on a printed page are a different kind of emergency waiting to happen.

How to build it without losing a whole weekend

You don’t need a perfect binder. You need an existing one. Done-and-imperfect beats planned-and-absent every time, so build it in passes:

- Pass one (20 minutes): Buy a real binder or create one cloud folder. Make the six section dividers. Fill in the one-page starter sheet above. Stop there — you now have something real.

- Pass two (one section at a time): Pick the section that scares you most — usually Money & Accounts or Medical — and spend 30 minutes gathering just that. A running list beats a perfect one. Tools like a bill tracker and a subscription tracker do the Money & Accounts section for you: every recurring charge, due date, and payment method already lives in one place, so you can print it straight into the binder.

- Pass three (the property layer): A home inventory spreadsheet (Google Sheets version here) handles the Home & Property section — it’s the single most useful thing to have ready before an insurance claim, and we make the full case for it in why every home needs a home inventory.

- Pass four (the medical layer): A medical expense tracker and a vital signs tracker turn the Medical section into a maintained record instead of a one-time guess — especially valuable if you’re helping an older relative, which we cover in how to talk to your aging parent about tracking their health.

The advantage of owning structured workbooks for the moving parts — bills, inventory, medical records — is that the binder stops being a snapshot you have to redo by hand every year. The sections that change the most maintain themselves, and you just print or export the current version.

Keep it alive: the 15-minute annual review

A family emergency binder isn’t a one-time project; it’s a living document. Accounts close, doctors change, kids age out of car seats and into college, and a policy you canceled is worse than no entry at all because it sends someone down a dead end.

Tie the review to a date you already remember — a birthday, New Year’s Day, or tax season — and give it 15 minutes once a year:

- Confirm every contact and account is still current.

- Remove anything you’ve closed or canceled.

- Add anything new: a policy, a property, a prescription, a person.

- Re-confirm your trusted person still knows where it is and how to get in.

That’s it. Fifteen minutes a year is the entire maintenance cost of never again leaving your family to reconstruct your life from memory.

The takeaway

A family emergency binder is the one file that lets someone step into your life and keep it running when you can’t. You don’t need to finish it today — you need to start it today, with a single page and two phone numbers. Build it in passes, store it in two places, tell one person it exists, and review it once a year. The reward isn’t a feeling of being prepared. It’s the very real gift of handing the people you love a manual instead of a mystery.

Disclaimer: This post is for informational and organizational purposes only and does not constitute legal, financial, tax, or medical advice. Estate documents, powers of attorney, and advance directives carry specific legal requirements that vary by state and by your personal situation — consult a licensed attorney, financial advisor, and your physician before finalizing decisions about wills, healthcare directives, or how your accounts and assets are handled.