The tag price is not your cost basis

The most common reselling mistake is treating the sticker you paid as the whole cost. A $4 Pyrex bowl set didn't cost you $4 to have ready to ship. It cost you the $4, plus the box and bubble wrap and tape and label you put it in, plus a slice of the gas you burned driving to three thrift stores to find it. That fuller number is the cost basis — and it's the only honest figure to measure a flip against.

Cost basis for a single flip is built from three parts:

- Purchase price. What you actually paid to acquire the item — the thrift, estate-sale or garage-sale price.

- Supplies. The packaging and prep that item consumed: poly mailer or box, bubble wrap, tape, the printed label, any cleaning or repair materials.

- A share of sourcing mileage. A sourcing trip rarely yields one item, so the trip's cost gets spread. If you drove 20 miles to find ten keepers, each carries a fair slice of that drive — valued at a per-mile rate, not ignored.

Why supplies and mileage belong in the number

Resellers leave these out because each one feels small. A mailer is "basically free." The gas is "a trip I'd take anyway." But these costs are real, they recur on every item, and they compound across a year of flips. Leave them out and your reported profit is inflated on every single sale — you're celebrating margin that the post office and the gas pump already took.

- Supplies are cost of goods, not overhead. A box you can't reuse is consumed by the sale, exactly like the item itself. It belongs in the item's cost.

- Mileage is a real cost of sourcing. The miles you drive to find inventory are generally treated as a business expense; assigning a share to each item makes your per-flip profit honest and keeps the record you'd need to support it. Exactly how mileage is deducted depends on your situation and current tax rules.

Cost basis is what stands between revenue and profit

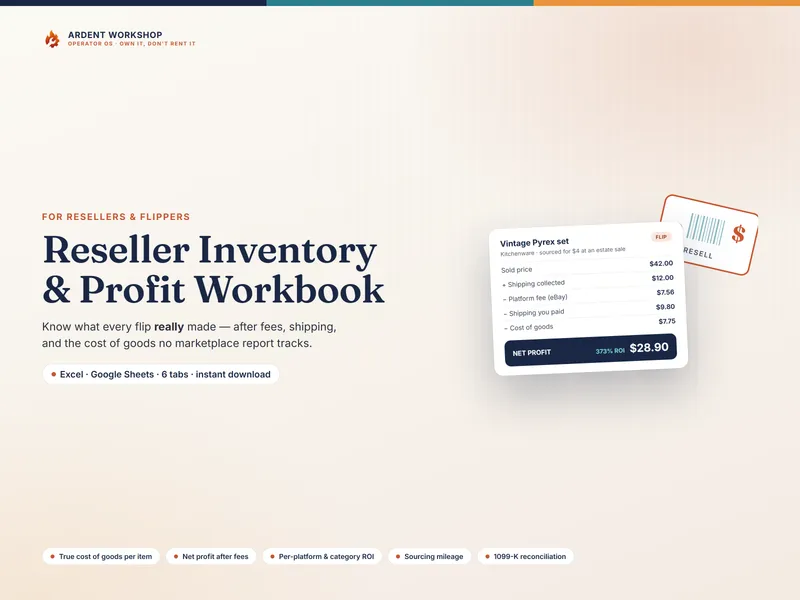

A sale isn't profit. The price a buyer pays runs a gauntlet before any of it is yours: the platform takes a fee, shipping takes its cut, and the item's cost basis comes out. What survives is net profit. Laid out in order:

- Sale price — what the buyer paid for the item.

- − platform fee — eBay, Poshmark, Mercari, Whatnot, Depop, Facebook or Etsy's cut, often a percentage plus a fixed charge.

- − net shipping — what you paid the carrier, minus any shipping the buyer paid you.

- − cost basis — purchase price + supplies + a share of sourcing mileage.

- = net profit — what's actually left for you.

ROI — net profit divided by cost basis — is the number that tells you whether sourcing that item was worth the trip. A small dollar profit on a tiny cost basis can be a spectacular ROI; a big sale price on an item that cost a lot to acquire and ship can be a poor one. You can run any single flip through the free Flip-Profit Calculator to see the fee, the net shipping, the cost basis and the profit without doing the arithmetic by hand.

Cost basis is also your 1099-K defense

Online marketplaces report your gross sales to the IRS on a Form 1099-K. That form shows the money that came in — not the money you spent to earn it. Without a record of what you spent, the 1099-K's gross figure is all you can show. Your cost basis is what you put against it: documented purchase prices, supply costs and sourcing mileage are the costs that bring "gross sales" down toward what you actually made.

This is why cost basis isn't just a profitability nicety — it's a record-keeping necessity. A reseller who logged the true cost of every flip through the year can reconcile the 1099-K line by line. A reseller who only tracked sale prices is reconstructing a year of thrift receipts from memory in April.

This explains how cost basis works for your records — it isn't tax advice. Reporting thresholds, business-versus-hobby rules, and how mileage and other costs are deducted differ by country, state and year and change often; confirm how they apply to you with a tax professional or your tax authority.

Common cost-basis mistakes resellers make

- Using the tag price as the whole cost. Covered above — the single biggest one, and it inflates profit on every item.

- Forgetting supplies entirely. Mailers, boxes and tape are a real, recurring cost of goods, not a rounding error.

- Ignoring sourcing mileage. The gas to find inventory is a cost — and a deduction — that vanishes if it's never assigned to anything.

- Confusing revenue with profit. A $42 sale is not $42 of income; the fee, the shipping and the cost basis all come out first.

- Keeping no record for the 1099-K. Without documented cost basis, gross sales look like taxable income at tax time.

Related templates and concepts

Cost basis is the reseller's version of cost of goods sold — the direct cost of what you sell — and it produces the profit margin that decides whether a flip paid. To see when a workbook is enough and when monthly reseller software earns its keep, read spreadsheet vs reseller inventory software, follow the how to track reselling profit tutorial, or browse every tool on the templates for resellers and flippers hub. You own the workbook outright — you don't rent it by the month.