On paper, the fixer-upper wins before you’ve even walked through the door. It’s the cheaper house on the same street — sometimes $30,000, $60,000, occasionally $100,000 below the move-in-ready listing a few blocks over. That gap is the single most persuasive number in the entire home search. It’s also the most misleading one you’ll see.

Here’s the honest version that never makes it into the listing: when you’re weighing a fixer-upper vs. a move-in-ready home, the discount isn’t savings. It’s an invoice you haven’t opened yet. The lower price is a real number, but it’s a down payment on work, time, disruption, and risk that the move-in-ready buyer already paid for — with cash, up front, in the price. Whether the fixer-upper is the smarter buy depends entirely on whether that hidden invoice comes out smaller than the discount.

Most buyers never actually do that math. They fall for one house, rationalize backward, and find out the truth eighteen months and three change-orders later. This post is about doing the math first — pricing the real trade-off, being fair to both sides, and then scoring the decision instead of agonizing over it.

The fixer-upper discount is not savings — it’s an unpriced invoice

A fixer-upper is cheaper because you are being paid, in the form of a discount, to do a job the seller didn’t. That job is a renovation, and renovations are notoriously bad at costing what you think they’ll cost.

The data here is not close. In a 2024 survey of 1,000 American homeowners, Clever Real Estate found that 78% went over budget on their last renovation — 44% by at least $5,000 and 35% by at least $10,000. And the overruns don’t spare people who “did it right”: in the same study, 53% of homeowners who hired contractors went over budget, versus 42% of DIYers. Hiring a pro buys you competence, not price certainty.

Scale matters too. Angi’s 2024 State of Home Spending report put average household spending on home projects at $12,050 for the year — and that’s the average across all homeowners, including people who did nothing more than repaint a bedroom. A gut renovation of a dated kitchen and two bathrooms lands in a very different bracket.

None of this means a fixer-upper is a bad buy. It means the discount has to be treated as a budget line, not a windfall. The right question isn’t “How much cheaper is it?” It’s “After I finish the work, will this house have cost me less than the move-in-ready one — including the parts I can’t put on a credit card?”

Where the fixer-upper discount actually goes

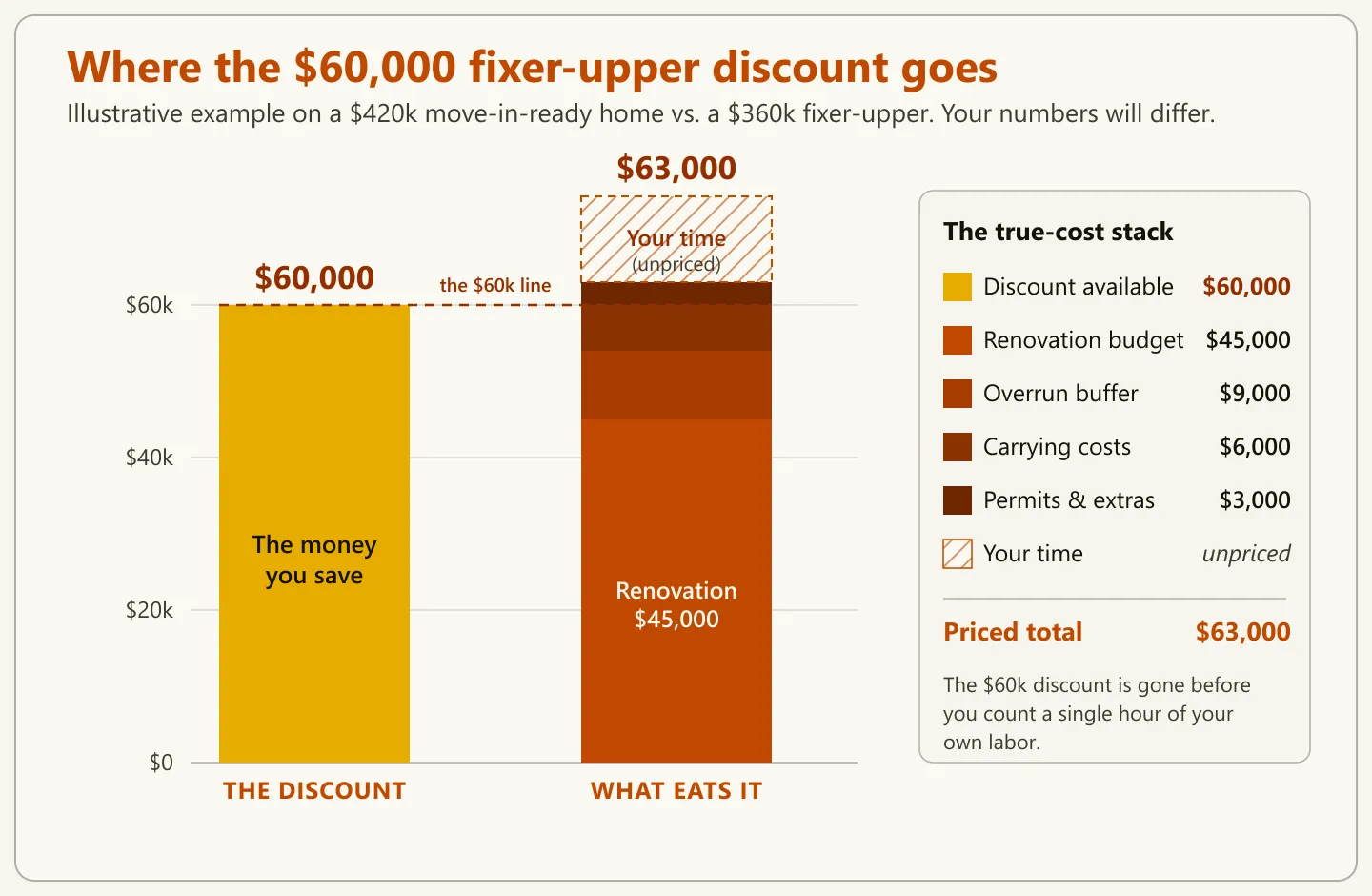

The discount gets consumed by four predictable costs, and a fifth that never shows up on a receipt. Let’s work through a deliberately simple, illustrative example — your real numbers will differ, but the shape of this is remarkably consistent.

Say you’re choosing between a move-in-ready home at $420,000 and a comparable fixer-upper on the same street at $360,000. The apparent discount is $60,000. Here’s where a realistic renovation sends it:

| Line item | Illustrative cost | Why it’s here |

|---|---|---|

| Renovation budget (kitchen, one bath, flooring, paint) | $45,000 | The actual scope you’re buying the house to fix |

| Overrun buffer (~20%) | $9,000 | Because roughly 4 in 5 renovations exceed budget |

| Carrying costs during the work | $6,000 | Rent/mortgage overlap + utilities on an unlivable house |

| Permits, inspections, dumpsters, financing extras | $3,000 | The small stuff that quietly adds up |

| Priced total | $63,000 | Already $3,000 past the discount |

| Your time and stress | Unpriced | Weekends of decisions, delays, and dust |

The punchline: the “$60,000 discount” is fully spent before you’ve assigned a single dollar to your own labor, lost weekends, or the stress of living in a construction zone. And this is the optimistic version — it assumes the walls hide no surprises.

That last line — your time — is the one buyers systematically zero out, and it’s often the most expensive of all. If you’d otherwise spend those months at work, with your kids, or simply not covered in drywall dust, that has a value. A renovation doesn’t fail only when it goes over budget in dollars. It fails when it goes over budget in the parts of your life you weren’t tracking.

Move-in-ready has hidden costs too — be fair to both sides

A move-in-ready home is not the “safe” choice by default; it carries its own hidden costs, and an honest comparison has to price them. Stacking the deck against the fixer-upper is just as expensive a mistake as ignoring its overruns.

When you pay the move-in-ready premium, you’re absorbing several real disadvantages:

- You pay for someone else’s taste — at retail. A flipped or freshly renovated home bakes the labor, materials, and the seller’s profit margin into the price. You’re buying finishes you didn’t choose at a markup you can’t negotiate down to cost.

- You inherit less equity upside. The classic wealth-building move in real estate is buying the worst house on a good street and improving it. A move-in-ready home has already captured that gain — for the seller.

- Turnkey homes attract bidding wars. Move-in-ready listings draw the largest pool of buyers, which is exactly the condition that pushes final prices above asking. The premium you see may not even be the premium you pay.

- “Renovated” is not the same as “renovated well.” Cosmetic flips can hide cheap work behind pretty surfaces. A fresh coat of paint over an old problem is a fixer-upper wearing a costume — and you paid the turnkey price for it.

- Opportunity cost of the extra cash. The dollars sunk into the premium are dollars not invested, not held as a cushion, and not available for the emergencies every homeowner eventually meets.

The takeaway is symmetrical: the fixer-upper hides its costs in the future, and the move-in-ready home hides its costs in the price. A good decision surfaces both.

The five factors that actually decide fixer-upper vs. move-in-ready

Strip away the emotion and the choice comes down to five factors. Score a fixer-upper honestly on each of these and the answer usually stops being a mystery.

- Budget headroom. Do you have renovation money that is genuinely separate from your down payment and your emergency fund — plus a 20% buffer on top? If the renovation budget only exists in theory, the fixer-upper isn’t a discount; it’s a debt trap with a nice foyer.

- Time and tolerance for chaos. Renovations run long and loud. Can you absorb months of decisions, dust, and delay without it wrecking your job, your relationships, or your sanity? Some people are energized by a project. Some are quietly destroyed by one. Both are valid — know which you are before you sign.

- Scope and structural risk. There’s a canyon between cosmetic (paint, floors, fixtures, a new kitchen) and structural (foundation, roof, electrical, plumbing, “we opened the wall and…”). Cosmetic scope is estimable. Structural scope is a coin flip with your bank account, and it’s where fixer-upper budgets go to die.

- Location and equity upside. The oldest rule still holds: the worst house on a great street is a better bet than the best house on a mediocre one. A fixer-upper in a location you couldn’t otherwise afford can be a genuinely brilliant financial move — the same house in a flat market is just work for its own sake.

- Financing reality. A conventional mortgage assumes a livable home. Financing a fixer-upper often means a renovation loan, a larger cash reserve, or carrying two housing payments at once. Sort out how you’ll pay for the work before you fall for the house that needs it.

For a deeper look at whether the timing and the numbers work for buying at all, our guide on whether you should buy a house this year walks through the affordability side before you ever get to condition.

Score the decision instead of agonizing over it

The reliable way to choose between a fixer-upper and a move-in-ready home is to score both against the factors you actually care about — with weights — and let the math surface the winner. This is the difference between a decision you can defend six months from now and a hunch you talked yourself into.

A weighted scoring system works in four steps:

- List your factors. Use the five above as a starting point, then add anything specific to you — commute, school district, yard, resale timeline.

- Weight them. Not every factor matters equally. If a short renovation timeline is critical because a baby is due in the fall, weight “time and chaos” heavily. If long-term equity is the whole point, weight “location and upside.” The weights are where your priorities enter the math.

- Score each home, factor by factor. Rate the fixer-upper and the move-in-ready home on each factor — say, 1 to 10 — using your real, researched numbers, not your first impression.

- Let the totals talk. Multiply each score by its weight, add them up, and compare. The winning home is the one that best serves what you actually said mattered — not the one with the prettiest kitchen or the scariest price tag.

Done on the back of a napkin, this collapses under the first hard trade-off. Done in a structured tool, it holds. This is exactly the job the House Buying Decision Helper was built for: you enter up to ten weighted factors, score each home against them, and the workbook produces an unbiased weighted score plus a breakdown of each home’s winning and losing factors. It’s a spreadsheet you own and reuse — for this house, the next one, and every big decision after — rather than a subscription you rent or a gut call you second-guess.

That’s the whole philosophy behind scoring a decision: you’re not outsourcing the choice to a formula. You’re forcing yourself to state your priorities before you walk into a house that’s going to make an emotional argument, and then holding the two homes to the same honest standard.

A gut-check before you sign for the fixer-upper

If your scoring points toward the fixer-upper, run this final checklist before you commit. Every “no” is a number you haven’t priced yet:

- I have a written renovation budget with a 20% buffer, held separately from my down payment and emergency fund.

- I’ve had a thorough inspection and, for anything structural, a specialist’s estimate — not a guess.

- I know where my family will live during the work, and I’ve priced that overlap.

- My financing covers the purchase and the renovation, confirmed with my lender.

- I’ve honestly assessed whether I can live through months of disruption — and whether my household agrees.

- I’ve compared the fixer-upper’s all-in cost to the move-in-ready home’s price, not its sticker to their sticker.

And once you own the place, the work doesn’t end at the renovation — it turns into upkeep. A seasonal home maintenance routine keeps the new kitchen from quietly becoming the next project, and a tool like the Home Maintenance and Warranty Log gives every appliance, contractor, and warranty a single place to live so the money you just poured in doesn’t leak back out through neglected upkeep or expired coverage.

The honest bottom line

Neither a fixer-upper nor a move-in-ready home is the “smart” choice in the abstract. The fixer-upper wins when its all-in cost — renovation, buffer, carrying costs, and your time — comes in below the move-in-ready price, and when you genuinely have the money, temperament, and timeline for the work. The move-in-ready home wins when certainty, speed, and a life without a construction zone are worth more to you than the equity you’re leaving on the table.

The mistake isn’t picking one. The mistake is letting a single seductive number — the discount, or the pretty finishes — pick for you. Price both sides honestly, weight what matters to you, score the two homes against the same standard, and buy the one the math actually points to. That’s how you fall for a house on purpose instead of by accident.

Disclaimer: This post is for informational and educational purposes only and does not constitute financial, tax, legal, or real estate advice. Every home, renovation, and local market is different, and the illustrative figures here are worked examples, not quotes — consult a licensed real estate agent, home inspector, contractor, and mortgage or financial professional before making decisions based on this content.