Restricted vs. unrestricted, in plain terms

Broadly, money a nonprofit receives falls into two kinds, defined by whether the donor attached a condition:

- Unrestricted funds. Money the organization can spend wherever the mission needs it — payroll, rent, the gaps nothing else covers. In current accounting language this is “net assets without donor restrictions.” Unrestricted operating support is the most valuable money a nonprofit can raise, precisely because it is flexible.

- Restricted funds. Money a donor or grantmaker tied to a specific program, project, or time period — “net assets with donor restrictions.” A grant for an after-school program can only be spent on that program; a gift designated for next year can only be used then.

Only the donor can place a restriction. Money the board sets aside for a purpose is board-designated, not restricted — the board can un-designate it at any time, so it is still unrestricted in accounting terms even though it is earmarked in practice.

A note on the terminology

Older guidance split restricted money into temporarily restricted (a time or purpose limit that will eventually lift) and permanently restricted (an endowment whose principal must be kept forever). Current U.S. nonprofit accounting standards simplified this into two buckets — with donor restrictions and without donor restrictions — though many people still use the older words in everyday conversation. Either way, the working idea is the same: track money by the strings attached to it.

Release from restriction

A restriction is satisfied — “released” — when the organization spends the money on what it was given for, or when the time limit passes. At that point the funds move from the restricted column into the unrestricted column in the books. Tracking releases correctly is what lets a nonprofit show a funder, and an auditor, that restricted money actually went where it was promised.

Why a small nonprofit has to track it

- It is a promise — and often a legal duty. Spending restricted money on the wrong thing can mean returning it, losing the funder, or a finding in an audit.

- Reporting depends on it. Most grants require a financial report showing what you spent against the grant budget. You cannot write that report if restricted spend was never tracked separately.

- It protects cash-flow decisions. An organization that treats its whole bank balance as spendable can find it has already committed money that was never really free.

Where small nonprofits go wrong

- Losing track of which dollars were tied to what — not from dishonesty, but from never recording the restriction when the money arrived.

- Spending against the wrong grant first when a cost could fairly be charged to more than one.

- Reconstructing spend at report time instead of keeping it current — a fund you keep current is a report you have already half-written.

- Overspending a restricted fund — a state a restricted fund should never reach, and one a simple running balance catches while it is still a rounding error.

A tracker is not your accounting system

A grant or fund tracker helps you see restricted balances at a glance and stay ahead of trouble — but it does not replace fund accounting in your books, and it is not financial, tax, or legal advice. How a grant is classified, which costs are allowable against it, and how restrictions are released are decisions for your finance team, your auditor, and each grant agreement. Use a tracker to plan and watch; reconcile it against your accounting records.

Related templates and concepts

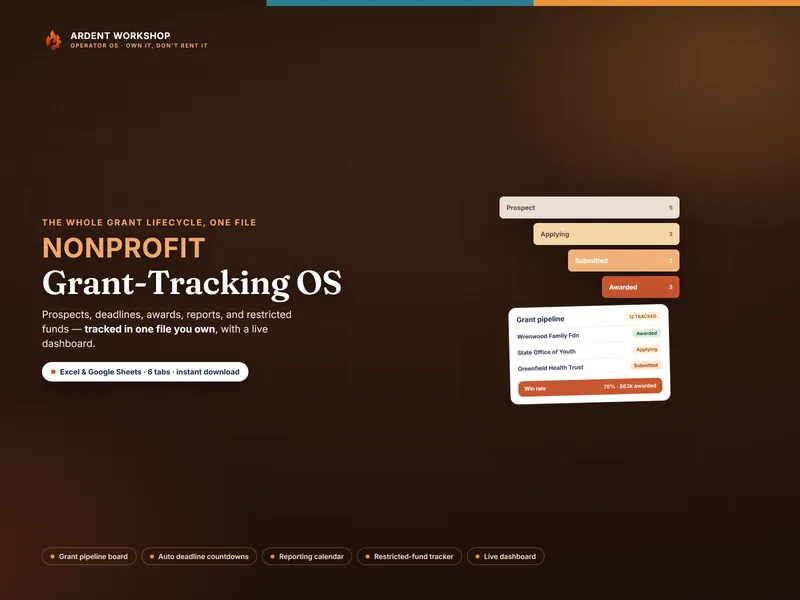

Restricted fund accounting is one piece of running a grants program. The free grant deadline tracker is an ungated taste; the full Nonprofit Grant-Tracking OS adds a restricted-fund tracker, a grant pipeline, and a reporting calendar in one owned workbook. Weighing tools? See spreadsheet vs grant management software, and the templates for nonprofits hub for the rest.