Markup is not margin — the mistake that underprices every job

One of the most expensive misunderstandings in the trades is treating markup and margin as the same number. They aren't.

- Markup is measured against your cost. Add 30% markup to a $10,000 job and you bid $13,000.

- Margin is measured against your price. On that $13,000 bid, your $3,000 profit is only 23% of the price — so a "30% markup" left you a 23% margin, not 30%.

If you need a 30% margin to keep the doors open and you mark up 30%, you come up short on every single job. The gap compounds quietly across a season of bids.

The formula that converts margin to markup

Decide the margin you need first — that's the percentage of revenue left after the direct cost of the work. Then convert it to the markup you have to charge:

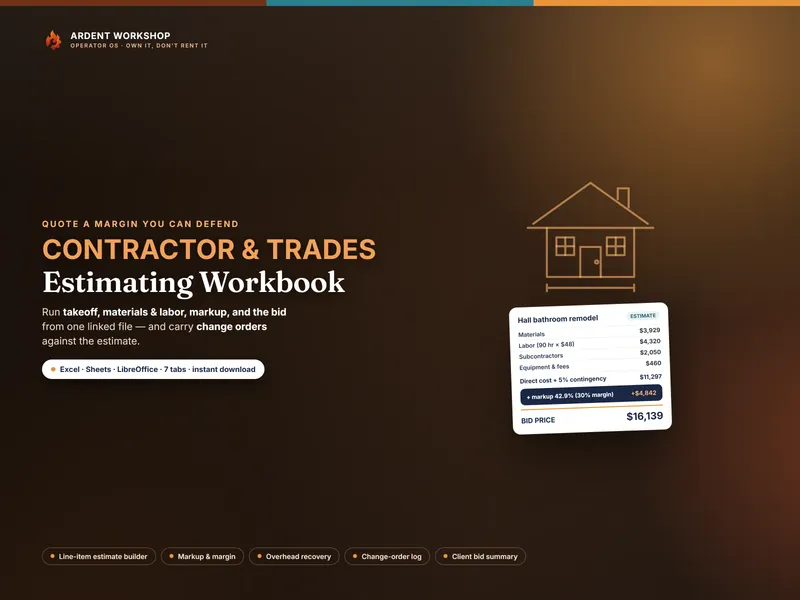

- Markup % = margin ÷ (1 − margin). For a 30% margin: 0.30 ÷ 0.70 = 42.9%.

- Price = cost ÷ (1 − margin). A $10,000 job at a 30% margin prices at $10,000 ÷ 0.70 = $14,286.

- Or use the multiplier: 1 ÷ (1 − margin). A 30% margin is a ×1.43 multiplier on cost.

A quick reference for the margins trades actually quote:

| Gross margin you want | Markup you must charge | Cost multiplier |

|---|---|---|

| 10% | 11.1% | ×1.11 |

| 20% | 25.0% | ×1.25 |

| 25% | 33.3% | ×1.33 |

| 30% | 42.9% | ×1.43 |

| 40% | 66.7% | ×1.67 |

| 50% | 100.0% | ×2.00 |

You can run any single job through the free bid-markup & job-cost calculator to see the price and margin without doing the arithmetic by hand.

What the markup actually has to cover

Markup isn't pure profit — it's the only place two real expenses get paid for:

- Overhead. The costs that exist whether or not you're on a job: your truck, insurance, tools, phone, software, the office, the hours you spend estimating and chasing payment. Spread a year of overhead across a year of jobs and you get the share every bid must carry.

- Net profit. What's left after the direct costs and overhead are paid — the reason the business is worth running.

A common mistake is marking up only enough to cover profit and forgetting that overhead has to come out of the same number. If your overhead runs roughly 20% of revenue and you want 10% net profit, the bid has to carry a ~30% gross margin — which, per the table above, is a 42.9% markup.

How trades set a markup

- Start from overhead, not a habit. "I always add 20%" is a guess. Add up a year of overhead, divide by the revenue you can realistically bid, and you'll know the floor your margin can't go below.

- Mark up every cost line, including subs and materials. Materials, loaded labor, subcontractors, equipment and permits all carry overhead and risk — marking up only labor leaves money on the table.

- Raise it for risk and hassle. Rush jobs, difficult access, finicky clients and fixed-price unknowns justify a higher markup, not a lower one.

- Price change orders at the same markup. Scope creep is where margin leaks. A change order is a small new job — bid it, don't give it away.

Common bid-markup mistakes

- Confusing markup with margin. Covered above — the single biggest one.

- Leaving overhead out of the markup. Then "profit" is really just paying for the truck.

- Marking up labor but not materials. A $6,000 material order with no markup is a $6,000 interest-free loan to the client.

- Forgetting to re-cost. Material prices move; last season's markup doesn't describe this season's lumber.

- Giving away change orders. "While we're here" is the most expensive phrase on a job site.

Related templates and concepts

Bid markup sits on top of cost of goods sold — the direct cost of the work — and it produces the profit margin that decides whether a job paid. To see when a workbook is enough and when dedicated job-costing software earns its keep, read spreadsheet vs job-costing software, or browse every tool on the templates for contractors hub.