Two PDFs are open on your laptop. Each one has a number in it. One number is bigger.

That is the entire comparison most people run, and it’s the reason this decision feels so much harder than it should. You sense that the bigger number isn’t automatically the better job, but the letter doesn’t give you anything else to weigh it against — so you read both documents nine times, ask three friends, and end up choosing on a feeling you’ll spend a year second-guessing.

Here’s what most people don’t realize about the document in front of you: the salary line is roughly two-thirds of what the job is actually worth. According to the Bureau of Labor Statistics’ Employer Costs for Employee Compensation report for March 2026, wages and salaries account for 69.9% of what private-industry employers spend on compensation, averaging $32.60 per hour worked. The other 30.1% — an average of $14.01 per hour — is benefits. That portion is real money spent on you, and almost none of it appears on the page you’re staring at.

So let’s pull the letter apart, put the missing third back in, and turn “which one feels right” into a number you can actually defend.

Why the Bigger Salary Isn’t Always the Better Offer

The bigger salary isn’t always the better offer because salary is the only part of compensation that’s easy to print, so it’s the only part that gets printed. Everything else — the premium your employer covers, the retirement match, the bonus odds, the cost of getting to the building — is either buried in a benefits summary you haven’t read yet or never written down at all.

This isn’t a rounding error. A gap of a few thousand dollars in base salary is routinely erased, and often reversed, by a difference in employer health contributions or a retirement match. Two offers that look $5,000 apart on paper can land in the opposite order once you count what each one actually delivers.

Regret is the predictable result of deciding without that information. In a 2022 survey of more than 2,500 workers, career site The Muse found that 72% had experienced “shift shock” — the surprise or regret of discovering a new job or company was substantially different from what they’d been led to expect. The survey skewed toward millennial and Gen Z workers during an unusually hot hiring market, so treat it as a signal rather than a law of nature. But the signal is worth taking seriously: a lot of people say yes to an offer and find out later they were comparing the wrong things.

The fix isn’t more agonizing. It’s counting the parts that weren’t printed.

What an Offer Letter Doesn’t Show You

An offer letter is a legal document, not a valuation. It exists to state a title, a salary, a start date, and the terms under which you can be let go. Four things that materially change what an offer is worth are usually missing from it.

The employer’s share of your health premium

Health coverage is the largest benefit most employers buy for you, and the amount they pay varies enormously between companies. In KFF’s 2025 Employer Health Benefits Survey, the average annual premium for single coverage was $9,325, of which workers contributed an average of $1,440 — meaning the employer covered about $7,885. For family coverage, the average premium reached $26,993 with workers paying $6,850, leaving employers covering roughly $20,000 a year.

Those are averages across all employers, and the spread around them is the point. One company paying 100% of your premium and another paying 60% of the same plan is a five-figure difference in what you’re being handed — and neither offer letter will mention it. Ask for the benefits summary and the per-paycheck premium cost for the specific plan you’d pick. That single document often decides the comparison.

The 401(k) match

A retirement match is money the employer contributes on your behalf when you contribute your own. Vanguard’s 25th annual How America Saves study (2026), which covers nearly five million retirement plan participants, reports that employer matching contributions have risen to a record 4.7% of pay.

Two details matter more than the headline number. First, the match only exists if you contribute enough to earn it — a 6% match is a 0% match to someone contributing 2%. Second, vesting decides whether you keep it. A generous match on a four-year vesting schedule is a retention device; if you’d leave in two years, half of it was never yours. Ask for the match formula and the vesting schedule together, because one without the other tells you nothing.

The bonus you might not get

A bonus described as “up to 15%” or “target 10%, discretionary” is not compensation. It’s a probability.

The honest way to count it is to multiply the target by the odds it actually pays, then ask the questions that establish those odds: What percentage of target paid out in each of the last three years? Is it tied to company performance, team performance, or a manager’s judgment? Is it prorated in your first year? A recruiter who can answer those crisply is describing a real bonus. One who reaches for “it’s always been strong” is describing a hope, and you should weight it accordingly.

What the job costs you to hold

Every job charges you something to show up. Commuting is usually the biggest line, and it’s the one people leave out most consistently.

The arithmetic is unforgiving. A 15-mile drive each way, five days a week, is about 7,200 miles a year once you net out vacation and holidays — call it 240 commuting days. At the IRS’s 2026 standard mileage rate of 72.5 cents per mile — the agency’s own estimate of what operating a vehicle costs, covering fuel, maintenance, insurance, and depreciation — that’s about $5,220 a year in real cost. (Commuting isn’t tax-deductible; the rate is just the most defensible per-mile figure available.)

Then there’s the part no rate captures. Forty-five minutes each way is 360 hours a year — nine forty-hour weeks of your life, unpaid, spent in a car. You don’t have to convert that to dollars for it to be a cost. You just have to stop pretending it’s free.

How to Calculate Total Compensation for a Job Offer

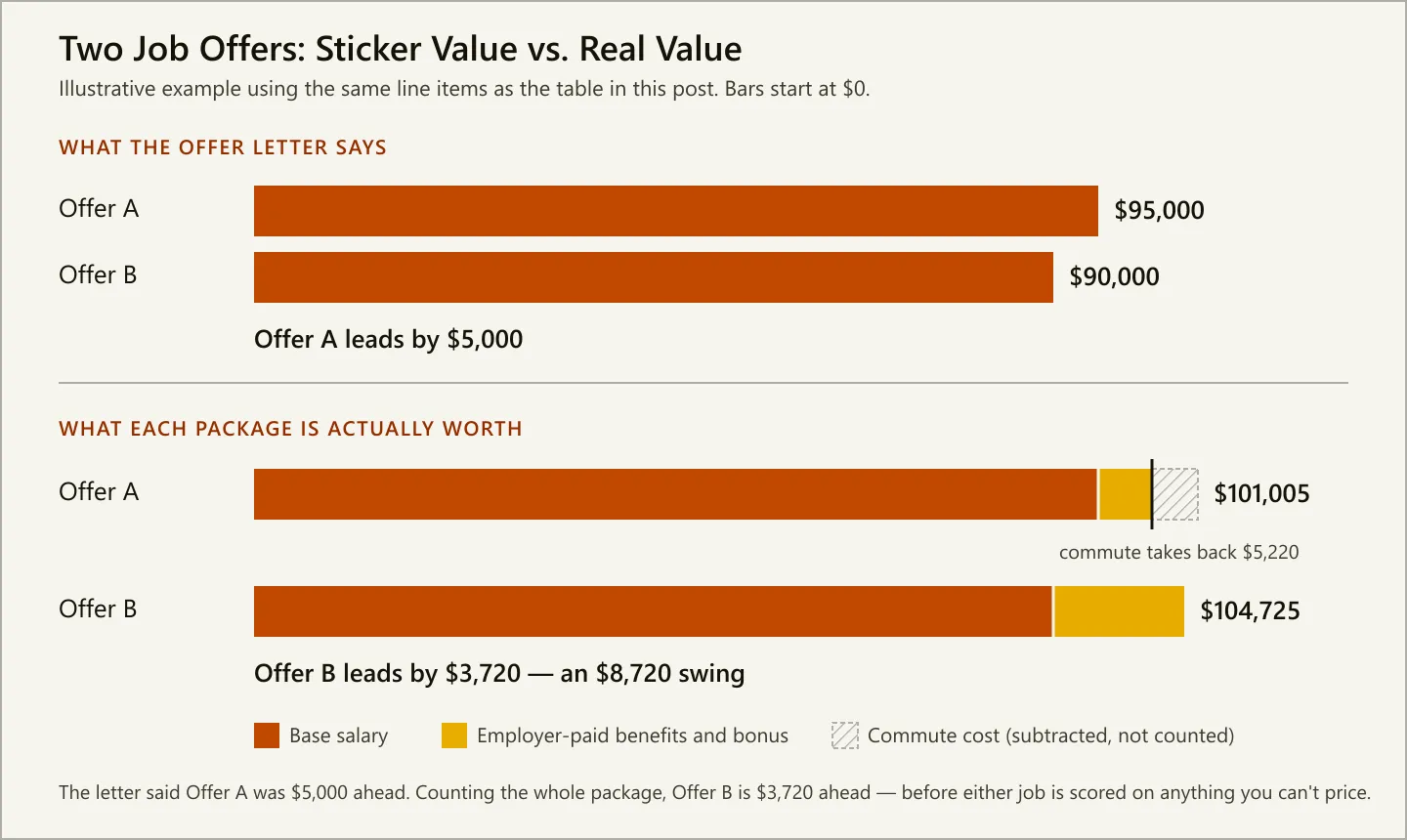

Total compensation is base salary plus everything the employer spends on you, minus what the job costs you to hold. Here’s how it plays out with illustrative numbers — the figures below are invented to show the shape of the math, not drawn from any real offer.

Picture two offers. Offer A pays $95,000, chips in $6,000 toward your health premium, matches 3% into retirement, dangles a 5% discretionary bonus that’s paid out about half the time, and sits 15 miles away. Offer B pays $90,000, covers your premium in full, matches 6%, offers no bonus, and is fully remote.

| Line item | Offer A | Offer B |

|---|---|---|

| Base salary | $95,000 | $90,000 |

| Employer’s share of health premium | $6,000 | $9,325 |

| 401(k) match (if you contribute enough to earn it) | $2,850 (3%) | $5,400 (6%) |

| Bonus, weighted by real odds (5% target, 50/50 history) | $2,375 | $0 |

| Gross package | $106,225 | $104,725 |

| Commute cost (7,200 miles at 72.5 cents) | −$5,220 | $0 |

| What the offer is actually worth | $101,005 | $104,725 |

That’s an $8,720 swing, and it came entirely from information that wasn’t in either document. Nobody had to negotiate, and neither company had to move a dollar — the reversal was sitting there the whole time, waiting for someone to add it up.

If you’d rather not do this on paper, the free Total-Comp Calculator runs the same arithmetic for two offers in your browser — no sign-up, nothing saved, and pre-loaded with an example where the higher base doesn’t win.

Two notes on doing this honestly:

- Don’t count paid time off as cash. Offer B’s 25 days versus Offer A’s 15 is a genuine difference, but you’re salaried — you get paid either way. Adding a dollar value double-counts your salary. Ten extra days is a lifestyle factor, so score it in the next section instead of smuggling it into the total.

- Don’t count equity at the number on the slide. Private-company equity is a lottery ticket with a strike price and a vesting cliff. Count it at zero, decide on everything else, and treat any eventual payout as a windfall rather than a plan.

The Parts of a Job Offer You Can’t Put a Dollar On

Once the money is settled, you’re left with the factors that actually determine whether you’re happy in eighteen months — and none of them have a price. That doesn’t make them unscoreable. It just means you supply the scale.

Five carry the most weight for most people:

- The manager. The single biggest predictor of how a job feels day to day, and the thing you have the most evidence about already. How did they answer when you asked what happened to the last person in this role? Did they describe their team as people or as resources?

- Growth and ramp. Does the role stretch you? A job you can already do is comfortable for a year and a dead end by year three. A job that’s a genuine reach costs you six months of feeling slow — and pays for a decade.

- Autonomy. How much of your day do you control? This is the difference between two identical titles at two companies, and it never appears in a job description.

- Stability. How is the company funded, and what did the last two years look like? A bigger number at a company with eighteen months of runway is a smaller number with extra steps.

- Flexibility. Remote, hybrid, core hours, the ability to disappear at 3pm for a school pickup. This is the factor people rank lowest during the interview and highest six months in.

The trap in scoring these is that it’s trivially easy to rig. If you already want Offer A, you’ll quietly hand Offer A a 5 on “growth” to make the total come out right. There’s one defense, and it’s the whole reason the method works: decide the weights before you score anything.

How to Score Two Job Offers Side by Side

This takes about half an hour, and it converts an argument you’re having with yourself into arithmetic you can check.

- Write down what you’re optimizing for — before you look at either offer. List the five to eight factors that matter to you this year, and give each a weight out of 100. Someone two years from a mortgage application weights cash heavily. Someone burned out weights flexibility and manager heavily. Both are correct; the mistake is not knowing which one you are.

- Add up each offer’s total compensation. Base, employer premium share, full match, bonus times its real odds. Use the table above as the template.

- Subtract what each job costs you to hold. Miles, parking, tolls, equipment, licenses, unreimbursed relocation.

- Score the unpriceable factors from 1 to 5. Use only what you observed — how the interviews were run, whether they started on time, what the team’s questions revealed, how fast they came back. Not what you hope is true.

- Multiply by your weights and total each column. The higher weighted total is the answer your own stated priorities produce. If it surprises you, that’s the method working — you’ve just learned something about what you actually want.

- Run the tiebreakers if the totals are close. More on that below.

To try the method before you build anything, the free Job-Offer Scorer does steps 1, 4, and 5 in your browser: weight five criteria, rate two offers 1 to 5 on each, and it returns one weighted score apiece. It’s pre-loaded with an example where the higher-paying offer loses, so you can watch the method work before trusting it with your own numbers.

The Job-Offer Decision Helper is the full version — up to four offers across eight criteria you choose, folding each offer’s money into one comparable total-comp figure and naming the gap between the best-fit and best-paid offer in real dollars. It’s a file you keep, which matters more than it sounds: you will make this decision again. The next offer, the internal transfer, the counter from your current employer three days from now. The weights you set today are the start of a record of what you actually value, and it’s yours — not a subscription you rent for a week and lose access to when you cancel.

If you’re weighing a bigger life pivot rather than two roles in the same lane, the same weighted-scoring approach scales up — the Decision Helper is the general-purpose version, and it’s worth reading how to organize a career change before you score anything.

What to Do When Two Job Offers Score Almost the Same

If the weighted totals land within a few points of each other, you’ve learned something genuinely useful: the offers are close, and you are not going to ruin your life either way.

That sounds like a non-answer. It isn’t. Most of the agony in this decision comes from an unexamined belief that one option is correct and the other is a mistake you’ll pay for — and a near-tie is evidence that belief is false. When the totals are close, use these in order:

- The regret test. Imagine turning each one down. One of them will produce a small flinch. That flinch is information your scoring rubric didn’t capture.

- The two-year test. Which decision would you still respect in two years, even if it didn’t work out? Not which one worked — which one was defensible with what you knew.

- The optionality test. Which offer leaves more doors open? The job that builds a rarer skill, or sits in a growing market, is worth a real discount on today’s cash.

- The counter. If one offer is close but behind on money, that’s not a tiebreaker — that’s a negotiation. Say so, to the company you’d rather join. A competing offer is the strongest and least awkward leverage you will ever have, and it expires the moment you accept. Handle it carefully, though; there’s a right way to ask, and it’s covered in how to negotiate salary without losing the offer. If you want the total-comp arithmetic and the counter-offer wording in one place, that’s what the Salary & Job-Offer Negotiation Toolkit is built for.

What not to do: don’t ask a fourth friend. You’ve already collected the information. Past a certain point, more opinions don’t produce clarity — they produce a wider spread of confident advice from people who won’t be doing the job.

Questions to Ask Before You Accept a Job Offer

Every question below exists to fill a specific hole in the math above. Ask them before you accept, not after — your leverage never gets higher than it is right now.

- What’s the per-paycheck premium for the plan I’d choose, and can I see the benefits summary?

- What’s the 401(k) match formula, and what’s the vesting schedule?

- What percentage of target bonus paid out in each of the last three years?

- Is the bonus prorated in year one?

- What happened to the last person in this role?

- What does the first 90 days look like, and who decides whether it went well?

- How many days on site, and is that policy written down or a current preference?

- Is there a written remote or relocation policy, or is this a handshake with my manager?

That second-to-last one does more work than it looks. “Written down or a current preference” is the difference between a benefit and a hope, and the answer tells you a lot about the company regardless of which it is.

The Decision You’re Actually Making

You’re not choosing between two numbers. You’re choosing which version of the next two years you want to be living, and the offer letter — the one document everyone stares at — was never designed to tell you that. It reports about 70% of the money and 0% of the rest.

So count the other 30%. Subtract what the job charges you to show up. Weight the things that don’t have a price before you score them, so you can’t cheat. Then read the total, and notice whether you’re relieved or disappointed — because that reaction is the last piece of data, and it’s free.

The people who spend a year second-guessing this decision are almost never the ones who picked wrong. They’re the ones who never wrote down what they were optimizing for, so they have no way of knowing whether they picked wrong. Half an hour of arithmetic buys you something better than certainty: a decision you can explain to yourself later.

Then accept it, close the laptop, and go be good at the job. What happens next is a different problem — and your first 90 days at a new job matter more than which offer you took.

Disclaimer: This post is for informational and educational purposes only and does not constitute financial, tax, legal, or investment advice. Benefit plans, match formulas, vesting schedules, bonus structures, and equity terms vary enormously between employers, and the right trade-off depends on your own finances, tax situation, and circumstances — consult a licensed financial advisor, CPA, or attorney before making decisions based on this content.