What Schedule E is for

If you rent out residential property — a single-family house, a duplex, a few units — the income and expenses are reported on Schedule E, which attaches to your Form 1040. It covers rental real estate (and a few other pass-through income types like royalties and partnerships). The idea is simple: report what the property earned, subtract what it cost to run, and carry the net income or loss to your return.

What goes on it, line by line

The form mirrors how a rental actually spends money:

- Rents received. The gross rent your tenants paid during the year — the starting figure, before any expense.

- Operating expenses, by category. Advertising, auto and travel, cleaning and maintenance, insurance, legal and professional fees, management fees, mortgage interest, repairs, supplies, property taxes, utilities, and a catch-all "other." Each has its own line.

- Depreciation. A yearly deduction that recovers the cost of the building and any capital improvements over time (see below).

- Net rental income or loss. Rents received minus every expense line — what the property made on paper for the year.

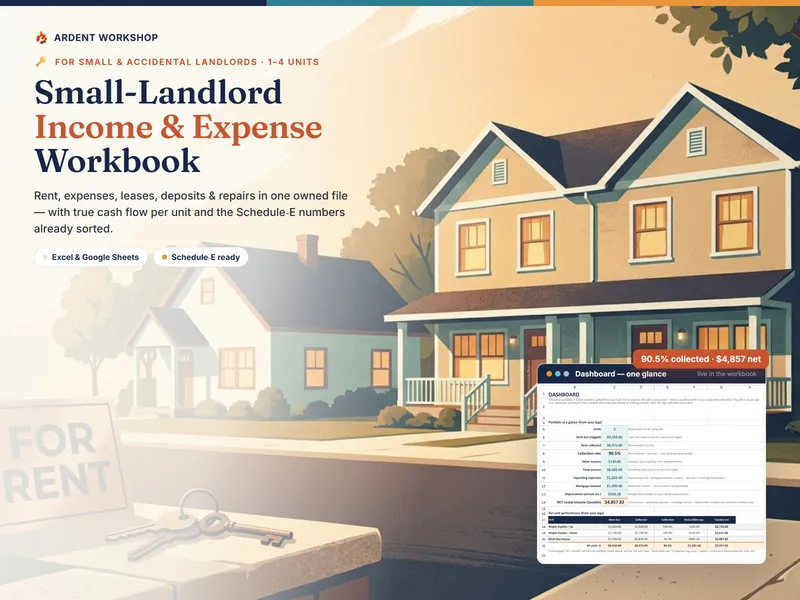

A workbook that tags every cost with its Schedule-E category as you go turns tax time from a shoebox reconstruction into reading a total off a tab. You can see the whole method in the Small-Landlord Income & Expense Workbook, or size up a single unit's cash flow with the free rental cash-flow calculator.

The two details that trip up new landlords

- Mortgage interest is deductible; the principal isn't. Only the interest portion of your mortgage payment is an expense on Schedule E. The principal is you buying the building, not a cost of running it — so a bank statement that splits the two matters at tax time.

- Repairs are deducted now; improvements are depreciated. A repair keeps the property in working order (a leak fixed, a broken latch replaced) and comes off this year's income in full. An improvement betters or extends the property (a new roof, a remodel, a new appliance) and is a capital cost recovered slowly through depreciation — for US residential rental property, over a 27.5-year recovery period under MACRS. Treating an improvement as a repair is one of the most common (and audit-prone) mistakes.

Schedule E vs. Schedule C

Most residential landlords report on Schedule E, where rental income is passive and isn't subject to self-employment tax. If you provide substantial services to tenants — the kind a hotel does, common with short-term rentals — the activity can instead be a business reported on Schedule C, where it may owe self-employment tax. Which one applies depends on the facts, and it changes the tax meaningfully, so it's worth confirming with a tax professional.

What Schedule E does not include

- Security deposits you're holding. A deposit is the tenant's money until you're entitled to keep it — it isn't rental income when you receive it.

- The mortgage principal. Not deductible, as above.

- Capital improvements, all at once. They enter through depreciation over years, not as a same-year expense.

A note on the rules

This is a plain-language overview, not tax advice. Passive-activity limits, personal-use rules, exactly how depreciation is figured, thresholds, and whether your activity belongs on Schedule E or Schedule C all depend on rules that change and differ by situation. Keep your receipts and confirm how they apply with a tax professional or the IRS.

Related templates and concepts

Keeping Schedule-E-ready records all year is what a landlord income & expense workbook is for. To decide whether a workbook is enough or you need dedicated software, read spreadsheet vs property-management software, or browse every tool on the templates for landlords hub.